Aware Super Review: Worth The Cost?

Last Updated on 20 February 2024 by Ryan Oldnall

Aware Super, Formerly First State Super is one of Australia’s largest industry superannuation funds. Aware Super has grown to have 1.1 million members and $125 Billion of combined assets as of May 2023 [1],[2].

In this Aware Super Review, I will discuss the pros and cons of Aware Super and discuss why I decided to switch away from them after 7+ years with the fund.

Who Are Aware Super Fund?

Aware Superannuation Fund was first established in 1992 for NSW Public Sector employees and their families. Aware Super opened up its membership to the wider Australian public in 2006. [2]

Aware Super like many large super funds has performed mergers throughout its history. In 2011, Aware Super Fund merged with Health Super and VicSuper in 2020.

In 2020, Aware Super changed its name from FirstState Super following its merger with VicSuper. This at the time made them the second largest super fund in Australia according to their own media release [3].

The rationale delivered at the time surrounding the name change was to help address the risk around climate change with the fund’s commitment to divesting from thermal coal by October 2022. Aware Super maintains its focus on socially conscious investments and offers several investment options to its clients.

Who Owns Aware Super?

Aware Super Pty Ltd serves as the trustee for Aware Super and holds ownership of Aware Financial Services and Aware Super Services. Additionally, they act as the issuer of superannuation and retirement products [4].

Similar to many other funds, Aware Super operates on a profit-for-member basis, prioritizing the goal of generating maximum profits for its members.

How Big Is Aware Super?

According to Aware Super, they currently have 1.1 million members as of May 2023 with $125 billion combined assets. For comparison, Australian Super had 3.06 million members and $274 billion under management as of December 2022 [4].

In terms of global ranking, Aware Super was found to be the 46th largest pension fund according to a worldwide study [6]. Again, for comparison, AustralianSuper Fund was found to be the 20th largest in that same study.

Aware Super Is An Industry Super Fund

As an industry super fund, Aware Super operates with the principle of not distributing dividends or profits as it does not have shareholders. Instead, all generated funds are reinvested back into the fund, to the benefit of its members.

This philosophy is similar to other Super Funds like AustralianSuper and Australian Retirement Trust Super, all of which are industry super funds.

Aware Super Fund has made significant strides to act on and address climate change within its investments. Aware Super believe they are able to act on climate change without impacting member returns, with tilts towards renewable energy investments.

Like other large funds, Aware Super has invested outside the square, investing in Tilt Renewables which is an Australian infrastructure investment fund. [1]

Aware Superannuation Review – Pre-Mixed Options

High Growth Option (Target 88% Growth / 12% Defensive)

The high growth option is an investment strategy designed to achieve robust long-term growth by diversifying its portfolio across a wide range of assets, with a specific focus on Australian and international shares.

As of May 11, 2023, the target allocation of the option was 25.5% in Australian shares and 42% in international shares.

This allocation indicates a strong emphasis on international exposure, showcasing a desire to capitalize on global market opportunities alongside the domestic market.

The fund’s primary objective is to surpass the Consumer Price Index (CPI) by more than 4% per annum over the medium to longer term, accounting for account fees, costs, and taxes.

However, it’s essential to note that due to the nature of high growth investments, there may be short-term fluctuations in returns.

Balanced Socially Conscious (75% Growth / 25% Defensive)

The socially aware investment option applies exclusions based on environmental, social, and governance (ESG) criteria to the Australian shares, international shares, and corporate securities within the fixed interest asset class.

Additionally, the private equity asset class allows for potential investments of up to 5% in companies and entities that do not meet the screening criteria.

This option overall is particularly suitable for investors seeking socially responsible investments with a focus on achieving strong long-term returns.The top portfolio allocations of the socially aware product are as follows: 21.5% in Australian shares, 35.5% in international shares, 10% in fixed income, and 9% in infrastructure and real assets.

The primary objective of the socially aware product is to outperform the Consumer Price Index (CPI) by more than 3.75% per annum over the medium to longer term.

While the product aims for medium- to long-term growth, it acknowledges the possibility of short-term fluctuations. It incorporates responsible investing principles through ESG screens with the ultimate goal of attaining competitive financial returns.

Balanced Option (Target 75% Growth / 25% Defensive)

The balanced investment option is strategically crafted to achieve medium- to long-term growth while being mindful of the possibility of short-term fluctuations.

The option offers a diverse portfolio that includes investments in shares, private equity, infrastructure, property, fixed interest, credit, and cash.

As of May 11, 2023, the primary target allocations were 21.5% in Australian shares, 35% in international shares, 10% in fixed income, and 9% in infrastructure and real assets.

The objective of the balanced option is to exceed the Consumer Price Index (CPI) by more than 3.75% per annum over the medium to longer term.

It is essential to consider that although the balanced investment option aims for growth, it recognizes the potential for short-term fluctuations.

As a result, it is structured to offer stability and moderate risk while pursuing medium- to long-term growth.

Conservative Balanced Option (Target 57% Growth / 43% Defensive)

The conservative balanced investment option is intentionally crafted to achieve medium-term growth while maintaining a careful balance between capital stability and capital growth.

While it seeks growth, it places a greater emphasis on fixed interest and cash allocations compared to the Balanced option, resulting in a more conservative investment approach.

The top portfolio allocations of the conservative balanced option include 15% in Australian shares, 24.5% in international shares, 17% in fixed income, and 14.5% in cash.

The primary objective of the conservative balanced option is to surpass the Consumer Price Index (CPI) by more than 2.75% per annum over the medium term.

Although the conservative balanced option aims for growth, it acknowledges the significance of capital stability and may experience some short-term fluctuations.

The emphasis on fixed income and cash strategically contributes to providing stability to the portfolio.

Balanced Index Diversified Option (Target 75% Growth / 25% Defensive)

The indexed diversified option utilizes indexing strategies to invest in a range of assets. Top asset allocations: Australian shares 28.5%, international shares 46.5%, fixed income 18%, and cash 7%.

This option aims for medium- to long-term growth, acknowledging short-term fluctuations.Primary objective: Achieve CPI + 3% per annum returns over the medium to longer term, generating real positive returns.

Indexing involves tracking specific market indices, providing broad market exposure and cost-effectiveness.

Note that slight variances may occur due to tracking errors or management fees despite aiming to match the selected index’s performance.

Aware Super Vs Australian Super Vs Australian Retirement Trust

Aware Super, Australian Super, and Australian Retirement Trust have well-established performance records that are comparable.

Each of these Superannuation funds offers comprehensive historical performance data, allowing us to assess and compare their performances over the past decade.

Throughout these comparisons diagrams Aware Super is referred to as ‘AW’, AustralianSuper as ‘AUS’, and Australian Retirement Trust as ‘ART’

These performance and fee-based figures are from published information on each Super funds website as of June 2023.

Aware Super Performance Comparison

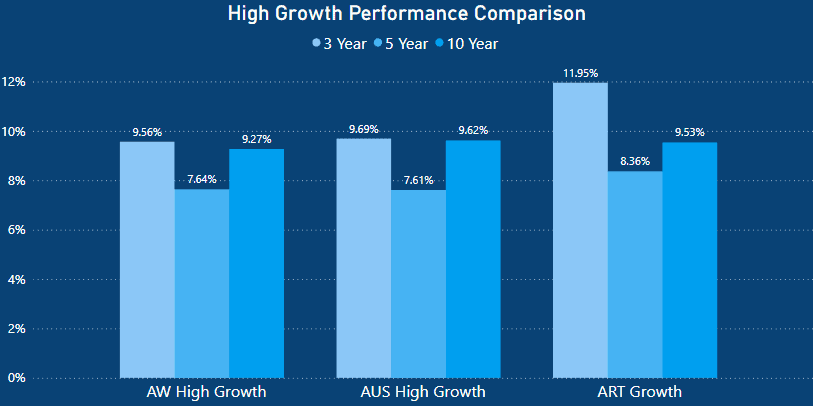

High Growth and Growth Options Comparison

When comparing the High Growth and Growth options, Australian Retirement Trust emerges as the clear winner in the short term (3 years), boasting an impressive 11.95% return. This result outshines Australian Super by 1.99% and Aware Super by 2.39%.

When looking at the medium term, Australian Retirement Trust remains the stronger performer with a return of 8.36%. This compares favourably to the similar performances of Aware Super and Australian Super who returned 7.64% and 7.61% respectively.

Over the longer term of 10 years, Australian Super has the best performance with a 9.62% return. This is that Aware Supers 9.27% and ARTs 9.53%

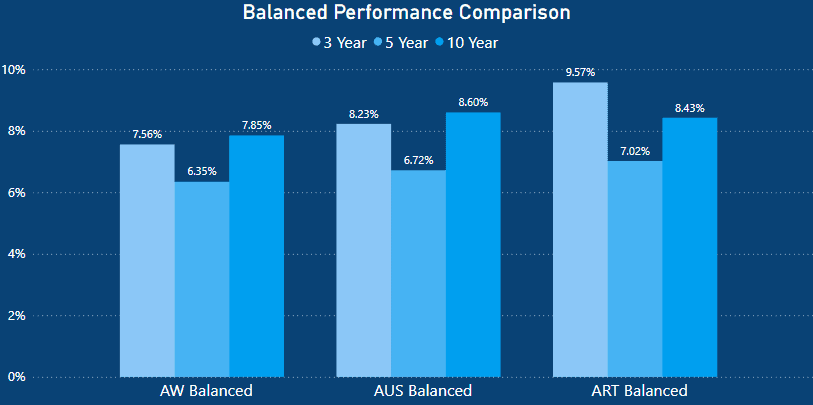

Balanced Growth Options Comparison

When evaluating the short-term 3-year performance of the balanced options among the three super funds, Australian Retirement Trust stands out as the clear leader with an impressive 9.57% return. Aware super returned a much lower 7.56% over the same period.

Over the period of 5 years, Australian Retirement Trust continued to have better performance returns. Australian Retirement Trust yielded 7.02% in comparison to Aware Supers 6.35% and Australian Supers 6.72%

However, when observing the 10-year performance record, Australian Super displayed the best performance, surpassing both Australian Retirement Trust and Aware Super. Australian Super returned 8.60% which was 0.17% more than Australian Retirement Trust and 0.75% more than Aware Super

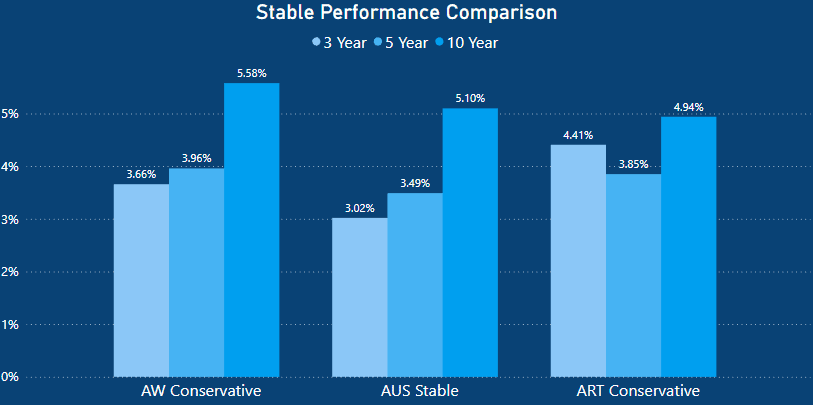

Conservative and Stable Options Comparison

Australian Retirement Trust continues to demonstrate outstanding performance in the short term when analysing a 3-year period. Their conservative option achieved a return of 4.41%, while Australian Super recorded the lowest return at 3.02%.

Moving on to the medium-term performances, the differences are somewhat comparable, with Aware Super performing the best at 3.96%, and Australian Super again having the lowest return at 3.49%.

Over the longer time frame of 10 years, Aware Super emerges as the clear top performer with an impressive 5.58%. This is followed by Australian Retirement Trust, 3.85% and Australian Super with 3.49%

Brief Explanation of Super Fees

Administration Fees: Super funds charge administration fees to cover the expenses of managing your super account, such as operating the call center and providing annual statements.

Administration fees may be structured as a fixed amount, a percentage of your account balance, or a combination of both, often with a maximum cap per year.

Investment Fees: Investment fees and costs (excluding performance fees) encompass direct and indirect expenses, including internal investment management costs, fees to third-party managers, custody expenses, derivative costs, and audit and administrative fees related to managing investments.

These costs contribute to the overall expenses associated with investment activities.

Transaction Fees: Transaction costs are additional expenses incurred by members who invest in a specific option.

These costs encompass various expenses related to buying or selling underlying investments, such as brokerage fees, settlement and clearing costs, stamp duty on investment transactions, and due diligence expenses.

Transaction costs for an investment option also include fees associated with individual members’ contributions, withdrawals, and switches between investment options.

The calculation of transaction costs is typically based on estimated expenses for a specific period, like the year ending on June 30, 2023. These costs are expressed as a ratio relative to the average value of all assets in the investment option during that period.

It’s important to understand that transaction costs can vary and are subject to change from year to year.

Performance Fees: Performance fees are an additional cost that goes beyond the regular investment and administration fees.

According to Aware Super’s Investment and Fees handbook, the Fund itself does not charge a performance fee directly. However, specific third-party investment managers may be eligible to receive performance fees when they achieve returns that exceed a specified benchmark.

In situations where these external managers do not perform well, no performance fees are payable.

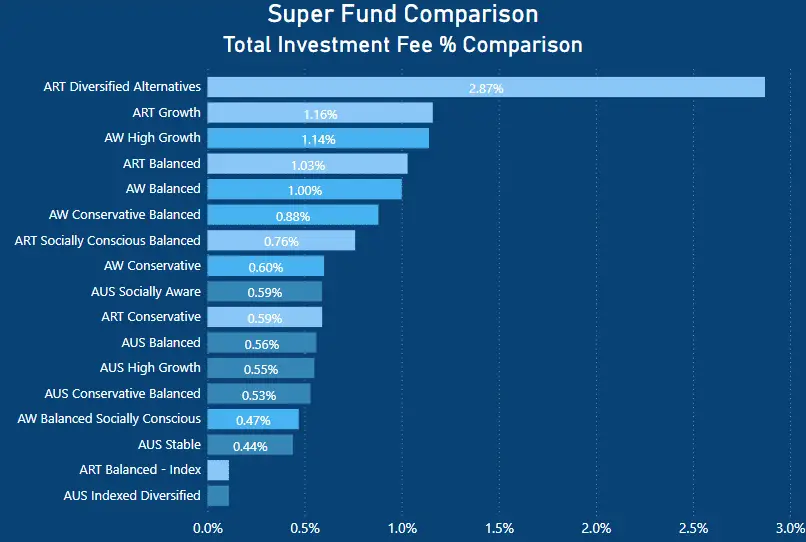

Fee Comparison: Investment Related Fees

When examining investment-related fees, it becomes evident that the fee amounts charged vary significantly based on the specific super fund product. n

Australian Retirement Trust’s Diversified Alternatives option stands out as a clear loser on the investment side, with a substantial fee of 2.87% being charged!

For their indexed option, both Australian Super and Australian Retirement Trust charge a fee of 0.11%.

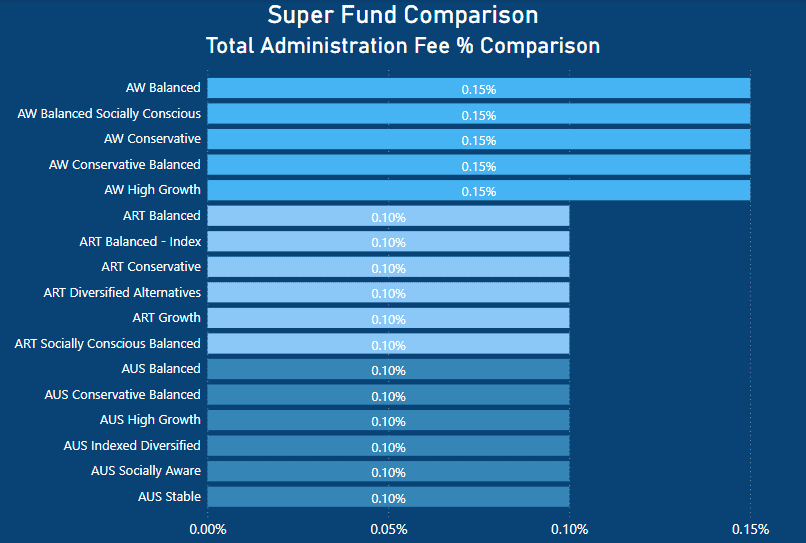

Fee Comparison: Administration Related Fees

Aware Super charges the highest administration fee percentage of 15%. Both AustralianSuper and Australian Retirement Trust charge 0.10% for administration related fees.

Fee Comparison: Total Related Fees

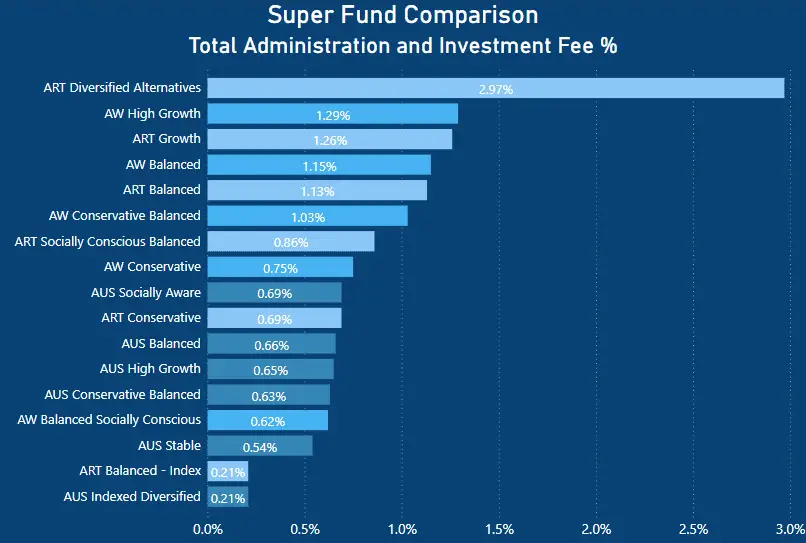

When examining the total fees charged, it comes as no surprise that Australian Retirement Trust’s diversified alternatives option is the most expensive, with a staggering fee of 2.97%!

- Australian Retirement Trust’s Growth and Balanced option charge 1.26% and 1.13% respectively.

- Aware Super’s High Growth and Balanced option charge 1.29% and 1.15% respectively.

- Australian Super’s High Growth and Balanced option charge 0.65% and 0.66% respectively.

Australian Super’s fees are significantly lower than that of both Aware Super and Australian Retirement Trust.

Let’s look at what this means in dollars for the average investor.

Fee Comparison: On a $50,000 Super Balance

When we examine a balance of $50,000, the annual costs show significant variation among the super funds. Australian Retirement Trust’s diversified alternatives have the highest cost at $1,547, and Aware Super’s High Growth option comes second at $697.

Looking at the growth and balanced options, Australian Retirement Trust’s growth option is $5 less expensive than Aware Super’s High Growth, totaling $692.

However, AustralianSuper’s high growth option is the most cost-effective at $377, resulting in an annual saving of $315-$320 compared to the others.

Similarly, for the balanced option, both Australian Retirement Trust and Aware Super charge $627, while AustralianSuper charges $382. Opting for the AustralianSuper balanced option allows for an annual saving of $245.

It’s essential to note that all three super funds apply an administration fee. They each charge an additional weekly dollar amount as part of their fees.

AustralianSuper and Aware Super impose a weekly fee of $1, whereas Australian Retirement Trust charges $1.20 per week. When evaluating the overall costs of the super fund options, these weekly charges should be taken into account alongside the administration fee.

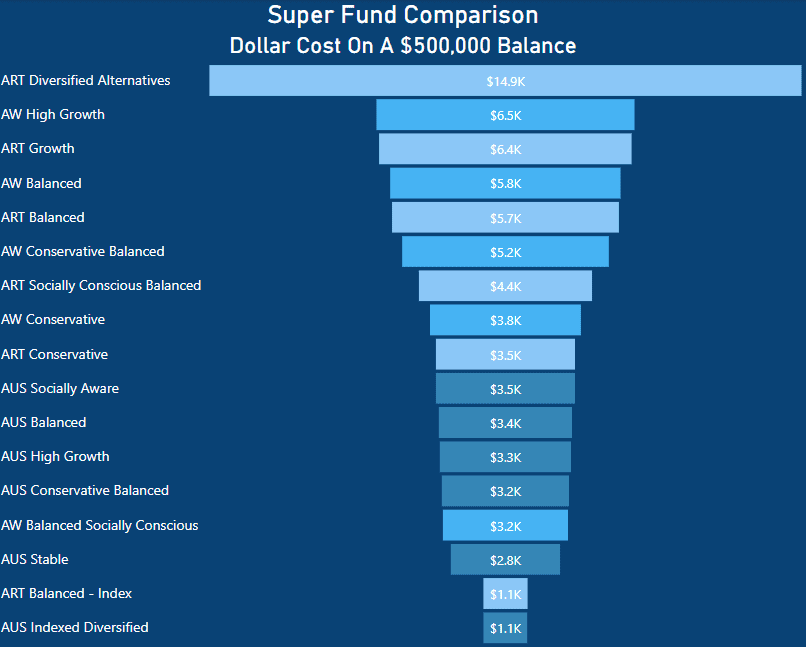

Fee Comparison: On a $500,000 Super Balance

When projecting this data to a $500,000 balance, the discrepancies in fees become even more significant. The annual fees for Australian Retirement Trust and Aware Super’s growth options surpass AustralianSuper’s High Growth option by $3,000 per year.

Likewise, for the balanced options, the fees of Australian Retirement Trust and Aware Super are approximately $2,300 higher than AustralianSuper’s balanced option.

While fees undoubtedly play a pivotal role in choosing a super fund, it is crucial to take into account all the aspects discussed in this review. Furthermore, seeking financial advice where appropriate is strongly advised to ensure well-informed decisions are made.

Aware Super Insurance

Aware Super offers insurance options within its products.

There are three types of insurance coverage available through Aware Super:n

- Total & Permanent Disablement (TPD) Cover: TPD Cover is designed to support you in the unfortunate event of a permanent disability that leaves you unable to work. It provides a lump sum payment.

- Death Cover: Death Cover ensures that if you become terminally ill or pass away, either you or your nominated beneficiaries will receive a lump sum payment.

- Income Protection: Income Protection provides regular payments to replace a portion of your income if you are unable to work due to illness or injury. The aim of Income Protection is to maintain financial stability during difficult times.

Should You Switch to Aware Super?

When considering a switch in super funds, it is crucial to approach the decision thoughtfully and ensure that your reasoning and rationale are well-founded.

In my research on this topic, I have written an article about the process of How To Choose A Super Fund

Aware Super has demonstrated robust performance over time, comparable to peers like Australian Super. Nonetheless, before considering switching super funds, there are several crucial factors to take into account:

Performance: Carefully assess the investment performance of the super funds you are considering. Analyze their historical returns and compare them against industry benchmarks.

While past performance does not guarantee future results, it can offer insights into how the fund has fared under various market conditions.

Fees and Charges: Thoroughly evaluate the fees and charges associated with each super fund, including administration fees, investment management fees, and other costs.

Lower fees can significantly impact your long-term returns, making it essential to understand the fee structure of the fund you are contemplating.

Investment options: Examine the variety of investment options offered within each super fund. Look for funds with a diverse range of options that align with your risk tolerance and investment objectives.

Insurance options: Check if the super fund provides insurance coverage, including life insurance, total and permanent disability (TPD) insurance, and income protection insurance. Evaluate the cost and extent of coverage to ensure it meets your needs.

Additional features and benefits: Explore supplementary features offered by the super funds, such as online account management tools, educational resources, financial planning services, and member discounts.

Consider which features align with your financial objectives.

Fund stability and reputation: Research the stability and reputation of the super funds under consideration.

Examine their track record, financial strength, and member satisfaction ratings. Factors like the fund’s size, longevity, and ability to consistently deliver returns over time should be considered.

Aware Super has made a dedicated effort to transition towards renewable and sustainable investments, a move that may resonate with the ethical considerations of certain investors.

Exit fees and insurance implications: Before switching super funds, be aware of any exit fees or penalties associated with leaving your current fund.

Additionally, consider the impact on your insurance coverage during the transition period, as most insurance policies have a waiting period before becoming active.

Review the product disclosure statement (PDS) provided by the superannuation providers to gather specific information about insurance coverage and waiting periods.

By being aware of any exit fees or penalties and understanding the insurance implications, you can effectively evaluate the potential costs and consequences associated with switching super funds.

Switching To Aware Super

In my article on How To Choose A Super Fund, I provide insights into why I decided to switch from Aware Super to AustralianSuper.

Initially, I had been with First State Super, and later this became Aware Super after the merger with VicSuper. I had been with them for over 7+ years, as they were the default super fund offered by my employer at the time.

However, during my research for these super fund reviews, I noticed a significant disparity in fees.

Aware Super charged considerably higher fees, and when accounting for insurance premiums, the costs became even more inflated.

This difference in fees was one of the key factors that led me to make the switch to AustralianSuper.

Furthermore, as highlighted in my Australian Super Review article, this AustralianSuper offers exposure to investment opportunities that are not easily accessible through other means.

Australian Super provides access to unlisted asset classes on a significant scale, making it an attractive long-term option.

Similarly, in my Vanguard Super Review, I discuss Vanguard’s highly competitive low fees, but ultimately, I decided against switching to their super fund.

While I acknowledged Vanguard’s super performance since its launch and its lower fees compared to AustralianSuper, the main reason behind my decision was that Vanguard’s Super Fund was only launched in October 2022.

Aware Super’s fees were just not competitive enough for me to stay with them. Having compared the dollar costs and how this would only increase over time prompted me to make the switch.

Aware Super performance in comparison to Australian Super did not justify the additional fees. Especially as Australian Super performances were better over 10 years than that of Aware Super.

Nevertheless, it’s important to remember that each individual has their own unique circumstances, and these should be taken into consideration when making any decision relating to super fund selection.

This article is for informational purposes only and does not constitute as an endorsement or recommendation to purchase any specific mentioned product.

- https://aware.com.au/member/become-a-member/what-it-means

- ,https://aware.com.au/about/cu,lture/history

- https://aware.com.au/content/dam/ftc/digital/pdfs/about/media/2020/Media%20Release%20-%20First%20State%20Super%20launches%20new%20brand%20-%20Aware%20Super.pdf

- https://www.australiansuper.com/campaigns/super-moments

- https://www.australiansuper.com/-/media/australian-super/files/about-us/media-releases/australiansuper-member-joins-increase-strongly-in-2019-20.pdf

- https://www.thinkingaheadinstitute.org/content/uploads/2022/09/PI-300-2022.pdf