Vanguard Super Review

Last Updated on 30 May 2024 by Ryan Oldnall

Vanguard Super is a relative newcomer to the Australian Super Fund market. Having announced its intention to launch an Australian superannuation fund back in 2020, Vanguard Super started in October 2022.

In this Vanguard Super Review, I will discuss the pros and cons of Vanguard Super and if I will be transitioning to its super fund in the future.

Who Are Vanguard?

If you haven’t heard of Vanguard, they are one of the world’s largest investment firms in the world. Founded in the US in 1975 they have 19 locations worldwide, 7 across the Americas, 8 in Europe, 1 in Asia and 3 in Australia [1].

Vanguard Group is not publicly traded and does not have a single owner or a small group of individuals who own it. Instead, Vanguard is owned collectively by the U.S.-domiciled funds and ETFs it manages.

This means that individuals who invest in these funds effectively become owners of Vanguard Group [2].

The ownership structure of Vanguard Group, where its investors collectively own the company, has consistently been attributed as the primary reason for its ability to maintain low and competitive investment fees.

This unique ownership arrangement aligns the interests of the group with its owners, as the company strives to prioritise the financial well-being of its investors.

How Big Is The Vanguard Group?

Vanguard is renowned globally for its extensive range of exchange-traded funds (ETFs) and mutual funds, managing an impressive portfolio of assets worth over AUD 11 trillion, worldwide.

In Australia, Vanguard Investments Australia oversees more than $104 billion in assets under management [2].

One of Vanguard’s most prominent offerings in the Australian market is the Vanguard Australian Shares Index ETF (VAS), which has gained significant popularity and holds the distinction of being the largest ETF in Australia.

Vanguard History in Australia

Vanguard have a solid investment history in Australia launching their first ETF in 2009. Vanguard has since launched several other ETFs and mutual funds which are hugely popular.

Vanguard is renowned for its collection of cost-effective exchange-traded funds (ETFs), and among them, Vanguard Australian Shares Index ETF (VAS) stands out as the largest ETF in Australia.

Vanguard’s reputation for low-cost ETFs extends beyond domestic markets, as they also offer individuals the opportunity to invest in international markets through their globally-focused ETF, VGS.

Vanguard MSCI Index International Shares ETF (VGS) provides exposure to a diverse portfolio of 1,500 companies worldwide. In fact, I covered the composition of VGS’ holdings in my article on diversification strategies for share investments.

Vanguard Super Fund

Vanguard Super launched in October 2022 after publicly announcing its intention to launch a Vanguard Super Fund back in 2020.

Vanguard’s current yearly fee for their My Super Lifecycle product is 0.58%. This fee is made up of 0.35% administration + 0.21% investment fee + 0.02% transaction fee. On a balance of $100,000, this would be $580 in yearly fees [3].

Vanguard Super provides a range of options for Australians, including their lifecycle product that incorporates age-based adjustments. The lifecycle product offered by Vanguard Super Australia automatically adjusts the investment strategy based on the individual’s age.

This means that as an investor gets closer to retirement, the allocation of their investments will gradually shift towards more conservative options.

This feature allows individuals to benefit from a tailored investment approach that aligns with their changing needs and risk tolerance over time.

Vanguard Superannuation Review – Pre-Mixed Options

Vanguard High Growth (90% Growth / 10% Defensive)

This investment option primarily focuses on assets with high growth potential, such as Australian and international shares.

Its main objective is to significantly increase your super balance over an extended period. However, it’s important to note that growth assets can be more volatile, leading to short-term negative returns.

Vanguard Ethically Conscious Growth (70% Growth / 30% Defensive)

If you prioritize ethically-conscious investments, this option might be suitable for you.

It aims to grow your balance in the long term while deliberately excluding companies involved in activities related to fossil fuels, alcohol, tobacco, gambling, weapons, nuclear power, and adult entertainment.

Vanguard Growth (70% Growth / 30% Defensive)

The Growth option offers a diversified investment portfolio across various growth assets, accompanied by defensive assets to protect your balance. Its main purpose is to foster the long-term growth of your investments.

By diversifying across growth assets, supplemented by defensive assets, this option aims to provide a balance between potential returns and risk management.

Vanguard Balanced (50% Growth / 50% Defensive)

With a focus on income assets, this investment option is designed to strike a balance between safeguarding your savings and minimizing the risk of negative returns. It offers a more equal distribution between growth and defensive assets.

Vanguard Conservative (30% Growth/ 70% Defensive)

This well-diversified option provides a blend of investments and is suitable for individuals seeking a balanced approach between income and capital growth within their portfolios. It leans towards a greater emphasis on defensive assets for risk mitigation.

Vanguard Super – Build Your Own Portfolio

Vanguard Super provides members with the flexibility to determine the allocation of their own superannuation investment. Vanguard offers a diverse range of sector-specific options that can be combined to build a personalized portfolio.

These options include Australian shares, international shares, hedged international shares, Australian fixed interest, hedged global fixed interest, and cash.

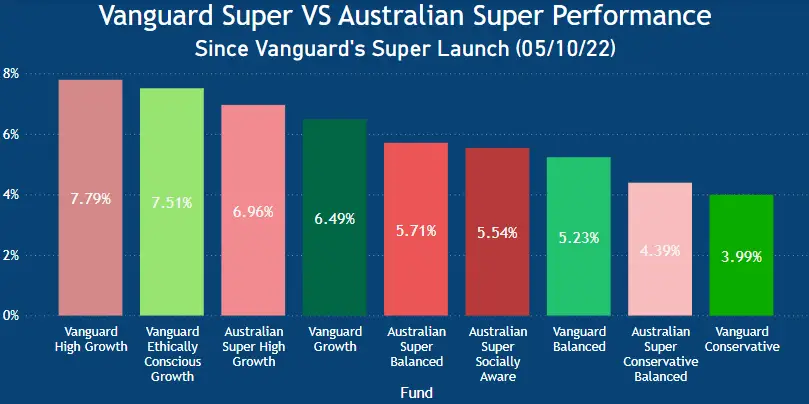

Vanguard Super Vs Australian Super

Vanguard Australia offers a limited breakdown of its performance, providing only four data points for evaluation.

These data points include performance figures since the product’s launch on 5 October 2022, as well as performance data for the past month, three months, and six months up until May 31, 2023.

In contrast, Australian Super provides a more comprehensive view of historical performance, offering data that extends down to the daily level. Using this data we will be able to compare performances since Vanguard’s launch.

For a more in-depth look at AustralianSuper’s performance read my latest Australian Super Review.

Vanguard Superannuation Performance Comparison

When it comes to performance, let’s compare Vanguard vs Australian Super. Looking at their performance history, vanguard super returns have met expectations and even surpassed Australian Super in some cases.

Vanguard’s High Growth super product has achieved a return of 7.79% since its launch, while Australian Super’s High Growth has returned 6.96%.

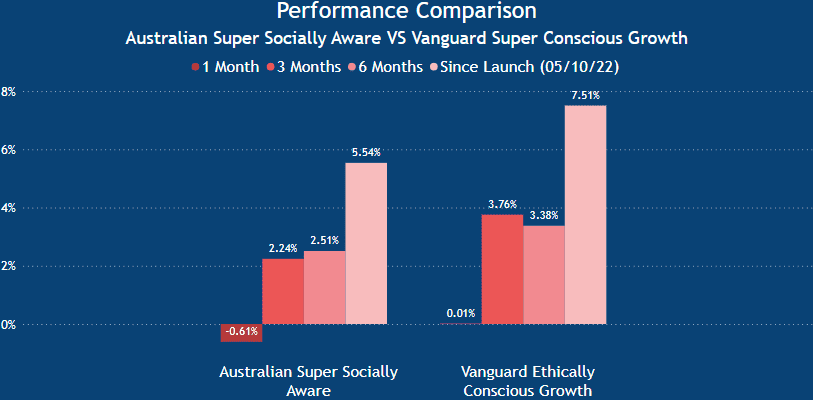

Interestingly, Vanguard’s ethically conscious fund has experienced growth of 7.51%, whereas Australian Super’s socially aware product has grown by 5.54%.

Performance Comparison: High Growth and Conservative Performance

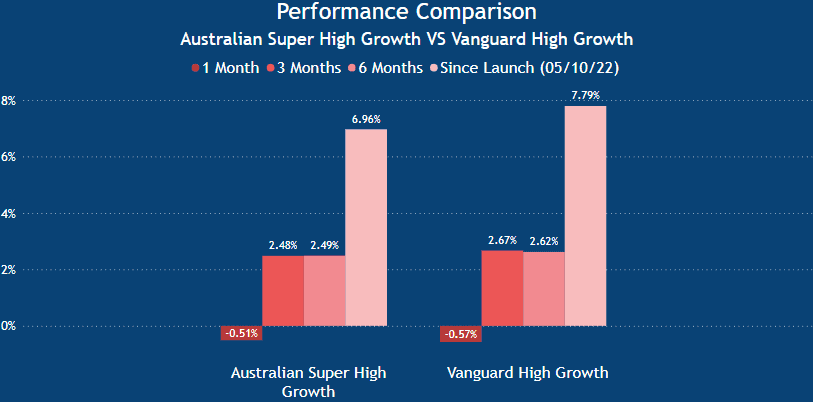

When analyzing the two ends of the investment spectrum, the results are very different for the high growth option. Australian Super has consistently lagged behind Vanguard in terms of performance for their high growth option, with a difference of only 0.13% over the past six months.

When comparing performance since October that gap between the high growth options increases to 0.83%.

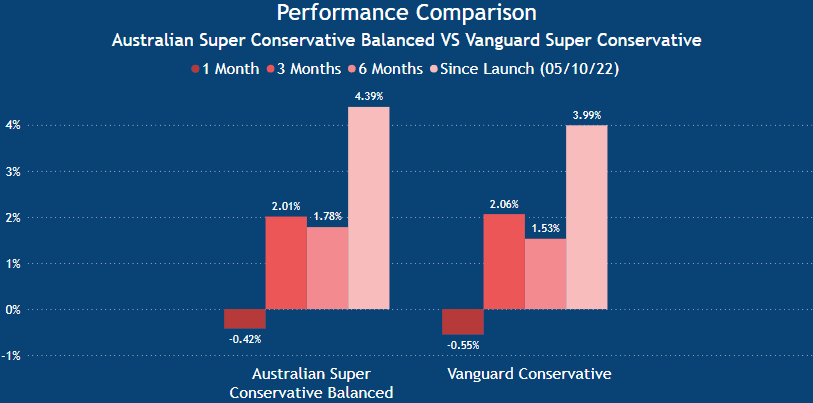

On the other hand, when considering the conservative funds, Australian Super has achieved a growth of 4.39% since Vanguard’s launch, slightly outperforming Vanguard’s 3.99%.

Performance Comparison: Balanced and Ethical Investing Performance

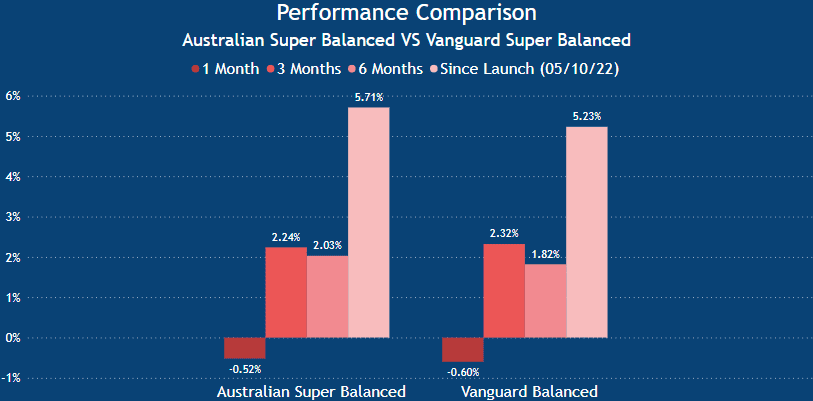

Over the past six months, Australian Super’s Balanced fund has outperformed Vanguard’s balanced fund by 0.21%. Since Vanguard’s launch, the margin in performance stands at 0.40%.

An intriguing observation is that Australian Super’s socially aware fund achieved a return of 5.54%, while Vanguard’s conscious growth fund returned 7.51% since its launch. Notably, this is only 0.28% lower than Vanguard’s high growth return for the same period.

It’s important to note that the available performance data for Vanguard is limited due to its launch in October 2022. As time progresses, a more comprehensive performance analysis can be conducted, providing a deeper understanding of its long-term performance.

Vanguard Australia Review Fee Comparison:

Super fees are a very important consideration when selecting a fund. Super costs will typically increase as your balance increases. The days of having a Super Fund charge 1%+ are gone, however,

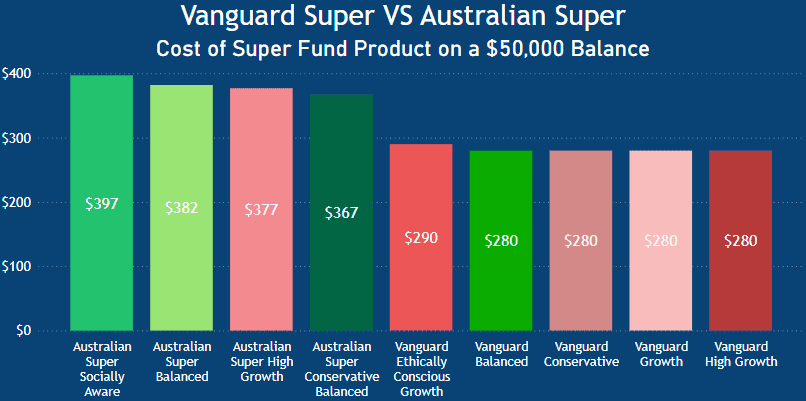

Low fee providers are out there and Vanguard Superannuation is one of them. When considering Vanguard Super fees, they charge on average $280 for their pre-selected options, with Australian Supers cheapest being $367 for their conservative balanced option.

Brief Explanation of Super Fees

Vanguard Administration Fees

Super funds charge administration fees to cover the overall expenses involved in managing your super account. These fees include costs like operating the fund’s call center and providing annual statements.

Administration fees can be structured as a fixed amount, a percentage of your account balance, or a combination of both. Many super funds set a limit, or cap, on the maximum total administration fees that can be charged in a year.

Vanguard charges an additional administration fee of 0.05% of your account balance per year to fund the Operational Risk Financial Requirement (ORFR).

The Operational Risk Financial Requirement is a regulatory requirement imposed on companies to ensure they have sufficient capital reserves to mitigate operational risks.

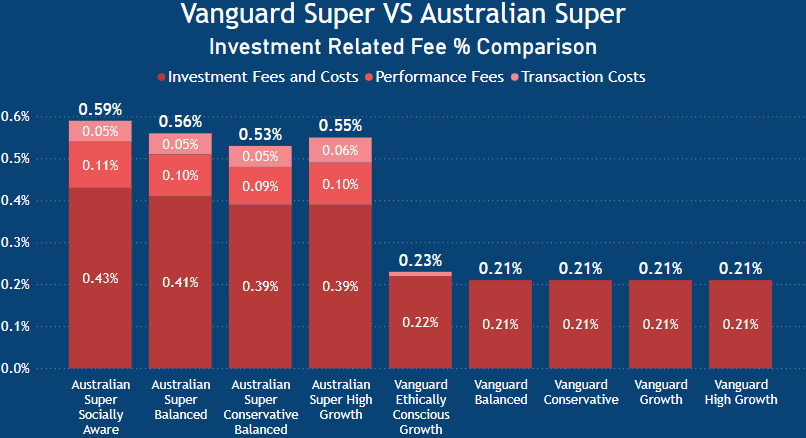

Vanguard Investment Fees

Investment fees and costs (excluding performance fees) include direct and indirect expenses.

These expenses consist of internal investment management costs, fees paid to third-party investment managers, custody costs, derivative costs, and audit and administrative expenses related to holding and managing investments.

They contribute to the overall expenses associated with investment activities.

Vanguard Transaction Fees

Transaction costs are additional expenses incurred by members who invest in a specific investment option.

These costs include various expenses related to the purchase or sale of the underlying investments, such as brokerage costs, settlement and clearing costs, stamp duty on investment transactions, and due diligence costs.

Transaction costs for an investment option also include expenses associated with individual members’ contributions, withdrawals, and switches between investment options.

The calculation of transaction costs is typically based on estimated expenses for a specific period, such as the year ending on June 30, 2023.

These costs are expressed as a ratio relative to the average value of all the assets in the investment option during that period.

It’s important to understand that transaction costs can vary and are subject to change from year to year.

Vanguard Performance Fees

Performance fees are an extra expense that goes beyond the previously mentioned investment fees and costs, as well as any administration fees.

While Vanguard does not have any listed performance-related fees, Australian Super does.

In Australian Super’s Product Disclosure Statement (PDS), they discuss that Australian Super does not directly charge a performance fee, but certain third-party investment managers may receive performance fees for achieving returns that surpass a benchmark.

Typically, these fees are calculated as a percentage of the investment returns that exceed a predetermined level of return. In many cases, there is an upper limit, or cap, on the percentage of investment returns that can be charged as a performance fee.

Vanguard Fee Comparison: Investment Related Fees

When comparing the investment-related fees of Australian Super and Vanguard, it is evident that Australian Super’s fees are significantly higher by 0.3% or more. It’s important to note that Vanguard does not charge a performance fee.

However, their ethically conscious product incurs a transaction fee of 0.02%.

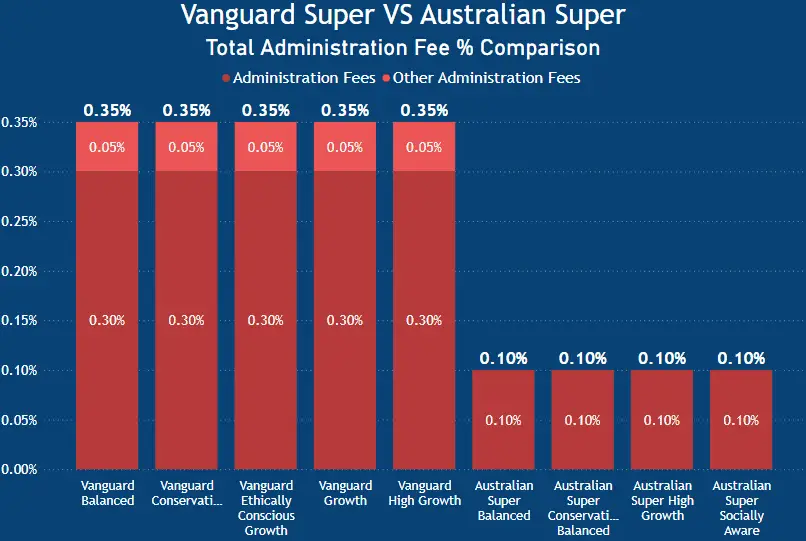

Vanguard Fee Comparison: Administration Related Fees

When comparing administration-related costs, Vanguard Super’s fees are higher than Australian Super’s. Australian Super charges an administration fee of 0.10% along with a flat fee of $1 per week.

In contrast, Vanguard charges an administration fee of 0.30% plus an additional 0.05% fee. Consequently, Vanguard’s total administration fees amount to 0.35% when compared to Australian Super’s 0.10% fee plus the weekly flat fee of $1.

Vanguard Fee Comparison: Total Combined Fees

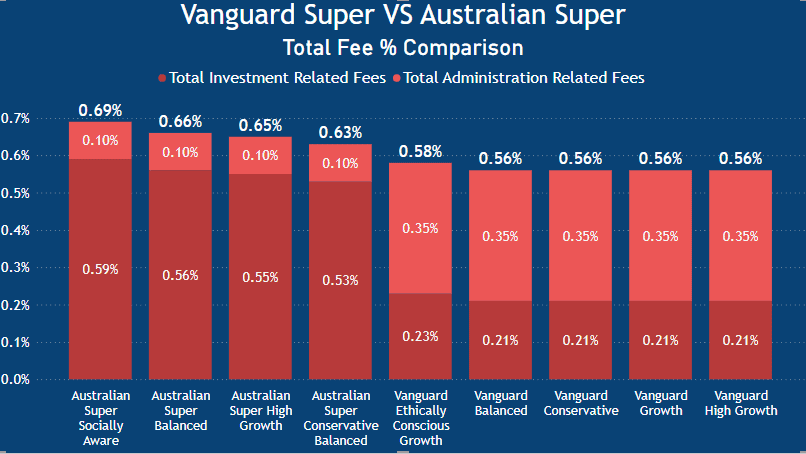

When evaluating the overall fees charged, both Australian Super and Vanguard offer competitive fee structures.

Australian Super’s highest fee is 0.69% for their socially aware product, while Vanguard’s average fee for their super products stands at 0.56%, with their ethically conscious option slightly higher by 0.02%.

In practical terms, both of these funds would fall into the category of low-cost providers, as other funds are considerably higher fees.

Vanguard Fee Comparison: On a $50,000 Balance

When evaluating the overall costs of individual super products, the disparity in fees becomes clear. Australian Super charges a market average flat fee of $1 per week, which is not calculated as a percentage of their administration fees.

Conversely, Vanguard offers significantly lower fees, resulting in Australian Super’s least expensive option being $87 higher compared to Vanguard.

Moreover, when comparing the highest-cost products for both the socially aware and ethically conscious options, the difference amounts to $107.

Vanguard Super Insurance

Vanguard superannuation offers insurance options within their products

There are three types of insurance coverage available through Vanguard Super:

- Total & Permanent Disablement (TPD): TPD Cover is automatically included in the default cover. In the unfortunate event of a permanent disability that leaves you unable to work, TPD Cover provides a lump sum payment.

It’s important to note that TPD Cover requires having Death Cover as well, and the TPD amount cannot exceed the Death Cover amount - Death Cover: Death Cover ensures that if you become terminally ill or pass away, either you or your nominated beneficiaries will receive a lump sum payment.

- Income Protection: Unlike TPD and Death Cover, Income Protection is not automatically included in Vanguard’s default cover.It provides regular payments to replace a portion of your income if you are unable to work due to illness or injury. Income Protection aims to maintain financial stability at certain times.

Should You Switch to Vanguard Super

When contemplating a switch in super funds, it is important to approach the decision with caution and ensure that your reasoning and rationale are well-founded.

In my exploration of the topic, I delve into the details of how to choose a super fund providing valuable insights.

Vanguard Super stands out for its low fees, which are prominently highlighted on its website. The company has a strong track record of delivering consistent value in the ETF space and has consistently provided favourable returns to investors.

It is essential to evaluate the following factors when considering a switch:

Performance: Evaluate the investment performance of the super funds you are considering. Look at their historical returns and compare them to industry benchmarks.

Remember that past performance is not a guarantee of future results, but it can give you an idea of how the fund has performed in different market conditions.

Given that Vanguard’s superannuation fund was launched in October 2022, it has a relatively short performance history of less than one year.

However, it’s worth noting that Vanguard has a long-standing track record of investing, which carries significant weight in evaluating its capabilities and expertise.

Fees and charges: Assess the fees and charges associated with each super fund. These may include administration fees, investment management fees, and other costs.

Lower fees can significantly impact your long-term returns, so it’s essential to understand the fee structure of the fund you’re considering.

In the case of Vanguard, it is evident that their fees and charges are notably lower compared to their major competitor, Australian Super. This cost advantage can potentially contribute to higher overall returns for investors over the long term.

Investment options: Consider the range of investment options available within each super fund. Look for funds that offer a diverse range of investment options to suit your risk tolerance and investment goals.

Some funds may provide a variety of asset classes, such as Australian and international shares, property, fixed interest, and cash. Vanguard offers several options that are well-suited for the average investor.

Vanguard provides pre-mixed diversified portfolios, allowing for a simplified approach to investing. Additionally, Vanguard offers a lifecycle product that adjusts the investment strategy based on your age, as well as the flexibility to build your own portfolio according to your preferences and risk appetite.

These options cater to a range of investment needs and offer opportunities for diversification and customization.

Insurance options: Check if the super fund provides insurance coverage, such as life insurance, total and permanent disability (TPD) insurance, and income protection insurance.

Evaluate the cost and coverage levels of these insurance options to determine if they meet your needs.

Extra features and benefits: Explore any additional features and benefits offered by the super funds. This may include online account management tools, educational resources, financial planning services, and member discounts.

Consider which features are valuable to you and align with your financial goals.

Fund stability and reputation: Research the stability and reputation of the super funds you are considering. Look into their history, financial strength, and member satisfaction ratings. Consider factors such as the fund’s size, longevity, and ability to deliver consistent returns over time.

As previously mentioned, Vanguard has a long-standing history of investing and is one of the largest investment firms globally. However, it’s important to note that as of May 2023,

Vanguard’s superannuation fund had 10,000 members and $500 million in funds under management, according to AFR.

In comparison, Australian Super boasts a significantly larger membership base of 2.4 million members and $233 billion in funds under management as of June 2021 [4]. These figures indicate the varying scales and scopes of the two funds.

Exit fees and insurance implications: Before switching super funds, understand any exit fees or penalties associated with leaving your current fund. Additionally, consider the impact on your insurance coverage during the transition period.

Most insurance policies have a waiting period before coverage becomes active, typically around 60 days.

It is advisable to review the product disclosure statement (PDS) provided by the superannuation providers to gather specific information about insurance coverage and waiting periods.

By being aware of any exit fees or penalties and understanding the insurance implications, you can effectively evaluate the potential costs and consequences associated with switching super funds.

Will I Switch To Vanguard Super

At this point in time, I have decided not to switch to Vanguard Super. I have several reasons for this decision that I will share. Firstly, I currently hold a diversified portfolio that includes Vanguard ETFs, among others.

I believe it would not be wise to have a significant portion of my future wealth concentrated in one company’s portfolio. While I don’t anticipate Vanguard disappearing overnight, I believe it is important to maintain some level of financial separation at this time.

Lastly, although Vanguard has a strong track record and a solid business foundation, its super fund has less than 12 months of performance history.

I would feel more comfortable making a switch if there were a 3-5 year track record available for comparison. Again, this comes down to risk appetite.

It is worth noting that Vanguard has outperformed Australian Super in certain product options but not in others. Having a longer track record would provide a more accurate basis for comparison.

Overall, Vanguard Super offers an attractive proposition with low fees and good performance to date. I am confident that it will continue to grow and attract new members.

Vanguard’s reputation has grown significantly over the past decade, thanks to its ETF portfolio, and I believe this will gradually attract more investors over time.

This article is for informational purposes only and does not constitute as an endorsement or recommendation to purchase any specific mentioned product.

1. https://www.vanguard.com.au/super/about-us

2. https://www.vanguard.com.au/adviser/en/aboutvanguard/about-us-tab

3. https://www.vanguard.com.au/super/performance-and-fees/calculate-super-fees

4. https://www.australiansuper.com/careers/our-teams