REST Super Review: The Right Choice For Retail Workers?

Last Updated on 3 March 2024 by Ryan Oldnall

Retail Employees Superannuation Trust (REST) has 1.9 million members and $70 billion in assets under management as of June 2023, making it one of Australia’s largest super funds on a membership basis [1].

In this REST Super Review, I will discuss Retail Employees Superannuation Trust’s performance, fees, and how it compares to the likes of Australian Super and Hostplus Super.

Who Are REST Super Fund?

Retail Employees Superannuation Trust was established in 1988. REST was first set up as a fund for those working in the retail sector. Since that time, like many super funds, it has opened its membership up to the wider public [2].

How Big Is REST Super Fund?

According to REST Super, they currently have 1.9 members as of June 2023 with $70 billion worth of assets under management [1].

For comparison, Aware Super has 1.1 million members and $125 billion under management [3], Hostplus has 1.7 million members and $100 billion funds under management [4], and Australian Super had 3.06 million members and $274 billion worth of assets under management [5].

In a comprehensive international study, worldwide pension funds were evaluated and ranked according to their size. Based on this global ranking, REST was evaluated as being the 121st largest fund globally.

For comparison, AustralianSuper Fund was found to be the 20th largest, Aware Super 46th and Hostplus 127th in that same study [6].

REST Super Is An Industry Super Fund

Industry superannuation funds, often known as profit-for-member funds, prioritize the financial well-being of their members. The fund’s primary objective is to make profits for its members.

REST Super is an industry super fund that abides by the fundamental principle of not distributing dividends or profits since it lacks shareholders.

Instead, all generated funds are reinvested back into the fund, ultimately leading to the benefit of its members.

This approach mirrors the philosophy embraced by other industry super funds, including AustralianSuper and Aware Super

REST Superannuation Review – Pre-Mixed Options

High Growth Option (88% Growth, 12% Defensive)

The High Growth Option serves as an investment strategy aiming to attain substantial and sustained long-term growth.

This is achieved by spreading investments across a diverse array of assets, with a specific concentration on shares from both the Australian and international markets.

Presently, the option’s strategic allocations are most heavily invested in shares, with 32% in Australian shares and 40% in international shares.

This distribution highlights an emphasis on international exposure. This underscores the intention to leverage opportunities in the global market in tandem with the domestic market.

The fund’s primary objective revolves around surpassing the Consumer Price Index (CPI) by a margin of 4% annually over the medium to extended term.

This accounts for associated fees, expenses, and taxes.

It’s worth noting, however, that due to the inherent nature of high growth investments, there could be short-term variations in returns.

Balanced Option (55% Growth, 45% Defensive)

The Balanced Option is crafted for medium- to long-term growth while acknowledging short-term fluctuations.

This option offers diversity through investments in shares, fixed interest, property, and infrastructure.

The current allocation prioritizes 16% in Australian shares, 21% in international shares, and 21% in fixed income.

The primary goal is to outperform the Consumer Price Index (CPI) by over 2% annually across the medium to longer term.

It’s important to consider that while growth is the aim, the option acknowledges the potential for short-term fluctuations.

The structure is designed for stability and moderate risk, pursuing medium- to long-term growth.

Capital Stable Option (38% Growth, 62% Defensive)

The capital-stable investment option aims for medium-term growth while reducing return volatility through strategic investments in fixed interest and cash.

It employs a diversified approach, investing across different asset classes using active, enhanced index, and index investment management.

This option emphasizes fixed interest and cash allocations more than the Balanced option, leading to a more conservative investment approach. It allocates 10% to Australian shares, 11% to international shares, 27% to fixed income, and 22% to cash.

The main objective of this conservative balanced option is to exceed the Consumer Price Index (CPI) by over 1% per year in the medium term.

Although the capital-stable option targets growth, it also values capital stability more so and might encounter short-term fluctuations.

The focus on fixed income and cash strategically contributes to portfolio stability.

REST Super Vs AustralianSuper and REST Super Vs Hostplus Super

REST Super, AustralianSuper, and Hostplus Super have established performance records that can be compared.

Each of these Superannuation funds provides comprehensive historical performance data, enabling us to assess and compare their performances over the past decade.

In the following comparison diagrams, REST is referred to as ‘REST,’ Hostplus as ‘HP,’ and AustralianSuper as ‘AUS’.

These performance and fee-based figures are information published on each Super funds website as of June 2023.

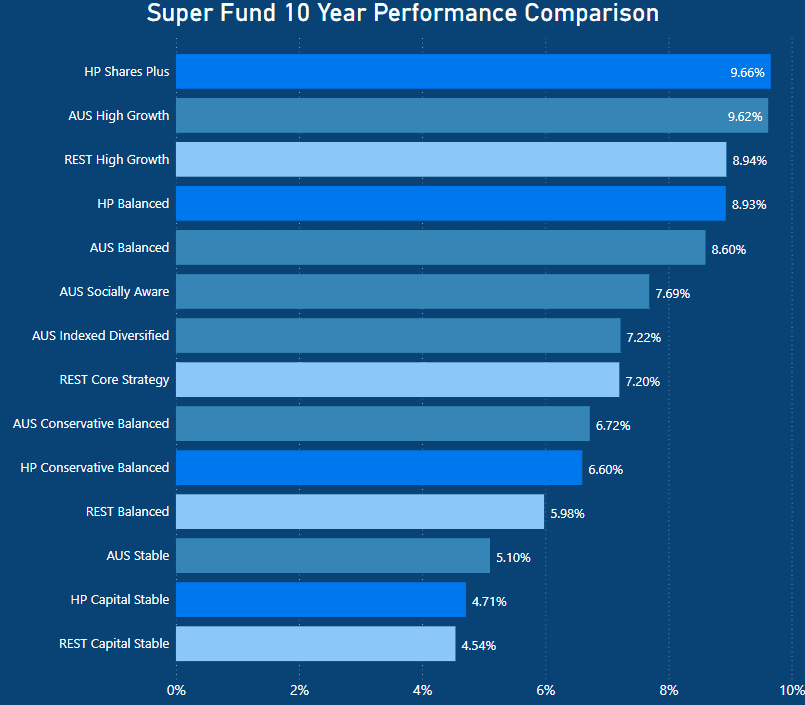

REST Super Performance Comparison

REST Super vs AustralianSuper and REST vs Hostplus Performance Over 10 Years

When we assess the performance of REST, AustralianSuper, and Hostplus Super over a decade-long period, it becomes apparent that the high growth option offered by Australian Super and Hostplus are the stronger performers.

Hostplus Shares Plus returned 9.66% whilst Australian Super returned 9.62%.

Australian Super’s high growth option exhibits impressive results with a notable return of 10.57%, surpassing its counterparts.

As anticipated, the stable options demonstrate lower performance due to their highly defensive nature.

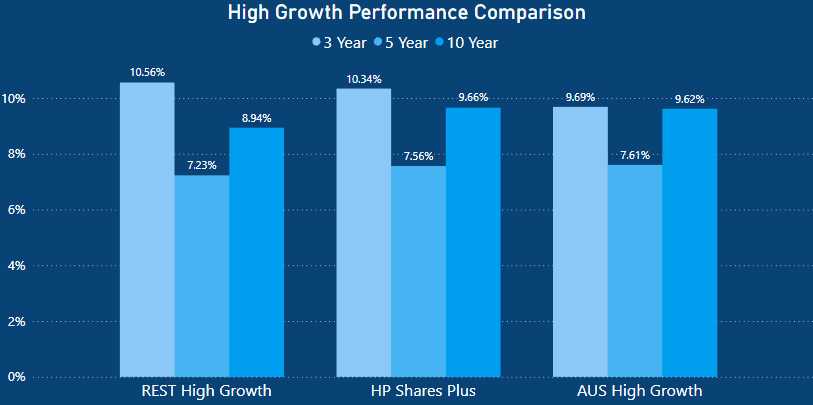

REST Super High Growth Option Comparison

When analysing the performance of REST’s high growth option, it exhibits a slight advantage as the more robust performer in the short-term.

Over 3 years, REST returned 10.56% whilst Hostplus and Australian Super returned 10.34% and 9.69% respectively.

However, over the medium to long term, AustralianSuper emerges as the strongest option. Over 5 years, Australian Super achieved a return of 7.61% on their high growth option, which is slightly higher than Hostplus’ 7.56% and REST’s 7.23%.

Similarly, looking at a 10-year period, Hostplus and AustralianSuper emerge the stronger performers. Hostplus returned 9.66% and AustralianSuper 9.62%. REST lagged behind with a return of 8.94% on their high growth. n

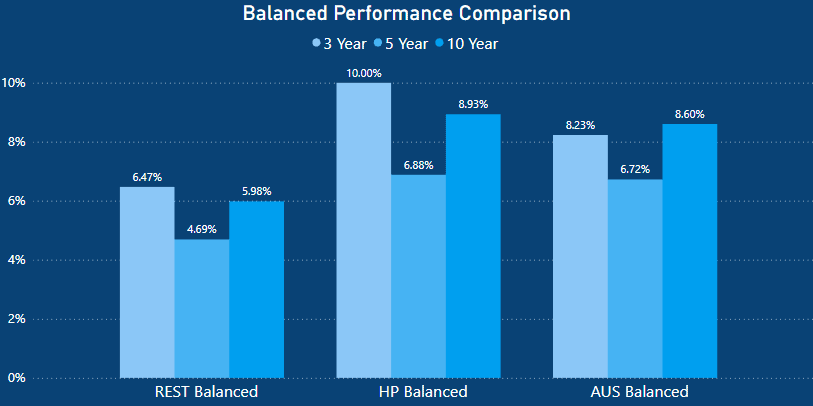

REST Super Balanced Growth Option Comparison

When examining the balanced option performances of the three funds, significant disparities in performance become evident, both in the short and long term.

This visual does not look good for REST’s balanced option. However, it’s important to note that REST’s balanced option is composed of 55% growth assets and 45% defensive assets.

In comparison, Hostplus is comprised of 74% growth assets and 26% defensive assets, while AustralianSuper consists of 66.3% growth assets and 33.7% defensive assets.

Consequently, a more equitable comparison can be drawn between Hostplus and AustralianSuper.

Over 3 years, Hostplus showcased superior performance with a return of 10%, outpacing AustralianSuper by 1.77%.

However, in the 5-10 year time frame, Australian Super closed the margin. However, despite this, Hostplus had the stronger performances over the 5-10 year period with returns of 6.88% and 8.93% respectively.

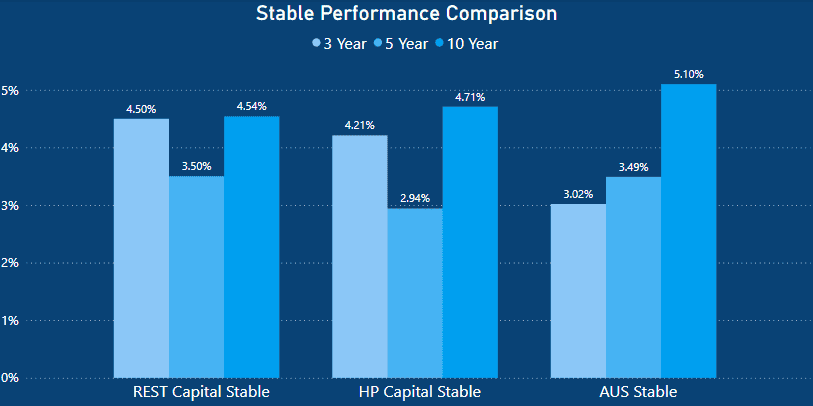

REST Super Capital Stable Option Comparison

REST’s capital stable option demonstrated comparable performance to that of Hostplus in the short-term span of 3 years.

REST yielded a return of 4.5%, while Hostplus returned 4.21%. This stood significantly better than Australian Super’s return of 3.02% over the same time frame.

Over 5-years, Australian Super’s performance picked up, achieving a return of 3.49%. In contrast, REST delivered 3.50%, with Hostplus decreasing to 2.94%.

Over 10 years, REST and Hostplus exhibited similar performance with their capital stable options. REST achieved a return of 4.54%, and Hostplus attained 4.71%. During the same period, Australian Super generated a return of 5.10%.

This performance was 0.56% better than REST and 0.39% superior to Hostplus.

Brief Explanation of Super Fees

Different types of fees are charged by super funds to account for various expenses linked with the management of your super account and investments. Here’s an overview of these charges:

Administration Fees: These charges are applied to offset the expenses associated with the management of your super account, which includes the operation of the call center and the provision of annual statements.

These fees can take the form of a fixed sum, a percentage of your account balance, or a combination of both, usually subject to an upper limit per year.

Investment Fees: Investment fees encompass both direct and indirect costs tied to investments.

This encompasses internal costs related to investment management, fees paid to external managers, custody outlays, derivative expenses, and audit and administrative charges linked to investment management.

These charges contribute to the overall costs incurred through investment activities.

Transaction Fees: Transaction expenses are additional costs borne by members who invest in specific choices.

These outlays encompass diverse costs associated with the purchase or sale of underlying investments, such as brokerage charges, settlement and clearing expenses, stamp duty on investment transactions, and due diligence costs.

They also include fees linked to individual members’ contributions, withdrawals, and shifts between investment alternatives.

Transaction costs are generally computed based on projected expenditures for a particular period, such as the year ending on June 30, 2023. They are expressed as a ratio relative to the average value of all assets in the investment choice during that time frame.

It’s crucial to observe that transaction costs can fluctuate and might alter annually.

Performance Fees: Performance fees are an extra expense in addition to the regular investment and administration charges.

Nonetheless, specific third-party investment managers might receive performance fees if they achieve returns surpassing a predefined benchmark.

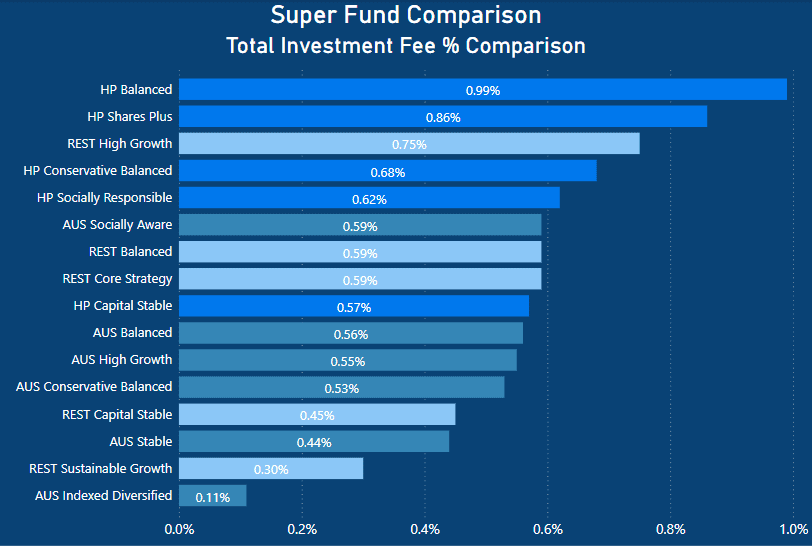

REST Fee Comparison: Investment Related Fee %

Upon analyzing investment-related fees, it becomes evident that the fee structures vary significantly based on the specific super fund option.

Hostplus stands out with the highest percentage-based fee for their balanced option among all the listed choices.

This exceeds the charges for REST and Australian Super’s balanced options by a considerable margin. Hostplus’ balanced option imposes a fee of 0.99% on their investment-related expenses, in contrast to REST’s 0.59% and Australian Super’s 0.56%.

Turning to the high growth options, once again, Hostplus emerges as the costliest with a fee of 0.86% for their shares plus option. In comparison, REST levies a fee of 0.75%, while Australian Super charges 0.56%.

Likewise, Hostplus applies the highest fee for their capital stable option, amounting to 0.57%. In contrast, REST and Australian Super charge 0.45% and 0.44% respectively for their equivalent option.

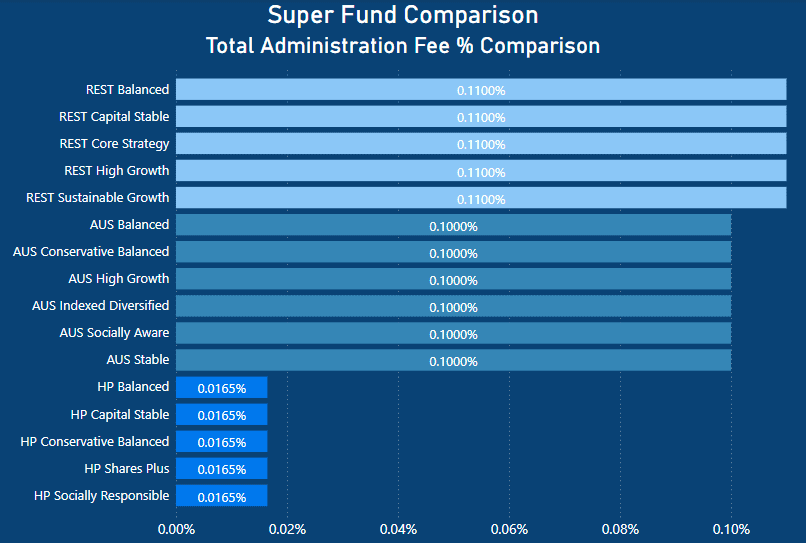

REST Fee Comparison: Administration Related Fee %

After examining the administration fee percentages, REST stands out with the highest percentage-based fees, imposing a 0.11% charge, which exceeds Australian Super by 0.01%.

Hostplus’ administration-based fee percentage is the Whcheapest, charging 0.0165%.

Nonetheless, alongside the listed administrative fee percentages, all three super funds apply additional fixed dollar-based fees.

AustralianSuper charge an additional $1.00 per week on top of their administration fee percentages.

Whereas, both Hostplus and REST charge $1.50 per week. However, Hostplus deducted an extra $32.91 per member from the fund’s administration reserve during the last financial year.

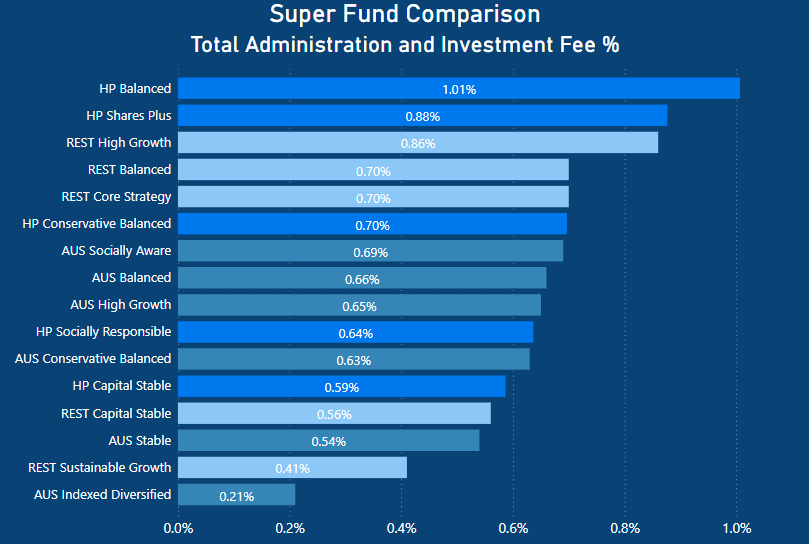

REST Fee Comparison: Total Fee %

When considering the overall percentage-based fees, Hostplus and REST emerge as the more costly choices. Combining both administration and investment-related fees, Hostplus charges a 1.01% for their balanced option. In contrast, REST imposes a 0.70% fee, while Australian Super adopts a fee of 0.66%.

Shifting to Hostplus’ high growth option, the fee stands at 0.88%, mirroring REST’s high growth option of 0.86%. AustralianSuper takes a more cost-effective approach, charging a lower fee of 0.65% for its equivalent product.

Lastly, when examining the stable capital options, all three options are very similar in their total fee percentages. Hostplus sets its fees at 0.59%, REST at 0.56%, and Australian Super at 0.54%.

Top 5 – Total Fee Related Percentages for High Growth, Balanced, and Stable Capital Options

- AustralianSuper Stable – 0.54%

- REST Capital Stable – 0.56%

- Hostplus Capital Stable – 0.59%

- AustralianSuper High Growth – 0.65%

- AustralianSuper Balanced – 0.66%

Next, let’s explore how these percentages translate into real dollar amounts for the average investor.

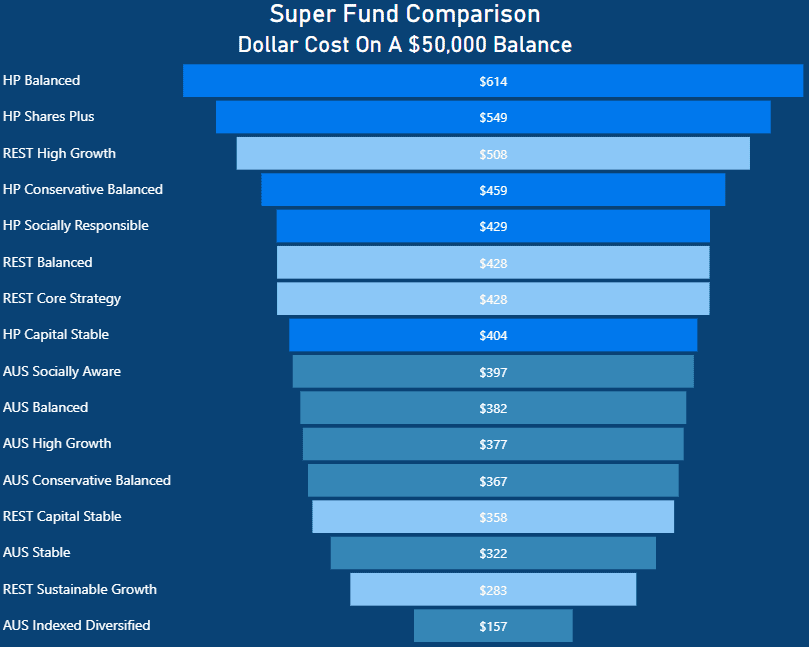

REST Super Fee Comparison: On a $50,000 Super Balance

The analysis of expenses associated with each Super Fund option reveals significant differences, especially when considering a balance of $50,000.

As anticipated, Hostplus charges the highest costs for their balanced and shares plus options, amounting to $614 and $549 respectively.

Within REST’s options, their most expensive is the high growth option, priced at $508 annually. Meanwhile, Australian Super charges a fee of $377 for their high growth investment.

As a result, this shows that Australian Super’s high growth option offers an annual savings of $131 in comparison to REST’s High growth. Similarly, REST’s balanced choice costs $428, while Australian Super’s stands at $382, and Hostplus’ remains the highest at $614 per year.

The Top 5 Cheapest – High Growth, Balanced, and Stable Capital Options on a $50,000 Balance

- AustralianSuper Stable – $322

- REST Capital Stable – $358

- AustralianSuper High Growth -$377

- AustralianSuper Balanced – $388

- Hostplus Capital Stable – $404

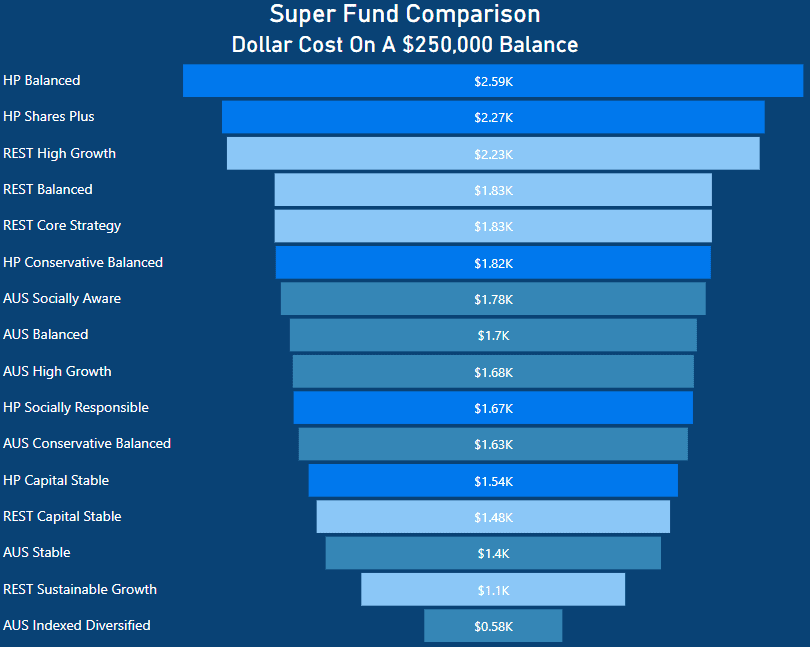

REST Fee Comparison: On a $250,000 Super Balance

When assessing a balance of $250,000, the disparities in fees become even more pronounced, owing to the application of percentage-based fees for each option.

Hostplus Super’s slightly higher fee percentages contribute to the widening gaps in fees for their more expensive options.

In the case of REST Super’s High Growth option, the annual fee would amount to $2,230, whereas Australian Super charges $1,680 and Hostplus charges $2,270. Australian Super is $550 cheaper than REST on an annual basis.

Turning to the balanced options, due to Hostplus’ high percentage fees, means they are the most expensive choice at $2,590 annually. This surpasses REST’s $1,830 and Australian Super’s $1,700 by a significant margin.

The Top 5 Cheapest – High Growth, Growth and Balance Options on a $500,000 balance

- AustralianSuper Stable – $1,400

- REST Capital Stable – $1,480

- Hostplus Capital Stable – $1,540

- AustralianSuper High Growth -$1,680

- AustralianSuper Balanced – $1,70

REST Insurance Options

REST Super presents a range of insurance choices available within its, product lineup. The insurance coverage provided by the fund encompasses three categories:

- Total & Permanent Disablement (TPD) Cover: If a lasting disability renders you incapable of working, this alternative provides a one-time payment.

- Death Cover: Opting for Death Cover means you or your selected beneficiaries will receive a lump sum payment in the event of terminal illness or death.

- Income Protection: This coverage ensures regular payments that substitute a portion of your income if you’re unable to work due to sickness or injury. Its purpose is to uphold financial stability during challenging circumstances.

Should You Switch to REST Super?

When contemplating a switch in super funds, it’s important to approach the decision thoughtfully and ensure your reasoning is well-founded.

In my research on this topic, I’ve written an article about the process of ,how to choose a super fund.

REST Super has shown consistent performance over time, comparable to peers like Hostplus

However, before you think about switching super funds, there are several key factors to consider:

Investment Performance: Carefully assess the investment performance of the super funds you’re looking at. Analyze their past returns and compare them with industry benchmarks.

While past performance doesn’t guarantee future results, it can provide insights into how the fund has performed under different market conditions.

Fees and Charges: Take a close look at the fees and charges associated with each super fund, including administration fees, investment management fees, and other costs.

Lower fees can have a significant impact on your long-term returns, so it’s important to understand the fee structure of the fund you’re thinking about.

Investment Options: Explore the range of investment options available within each super fund. Look for funds that offer a variety of options that match your risk tolerance and investment goals.

Insurance Coverage: Check if the super fund provides insurance coverage, including life insurance, total and permanent disability (TPD) insurance, and income protection insurance. Evaluate the cost and coverage to make sure it fits your needs.

Additional Features and Benefits: Look into extra features offered by the super funds, such as online account management tools, educational resources, financial planning services, and member discounts. Consider which features align with your financial objectives.

Fund Stability and Reputation: Research the stability and reputation of the super funds you’re considering. Examine their track record, financial strength, and member satisfaction ratings.

Factors like the fund’s size, longevity, and ability to deliver consistent returns over time should be taken into account.

Exit Fees and Insurance Implications: Before switching super funds, be aware of any exit fees or penalties associated with leaving your current fund.

Also, consider the impact on your insurance coverage during the transition period, as most insurance policies have a waiting period before they become active.

Review the product disclosure statement (PDS) provided by the superannuation providers to gather specific information about insurance coverage and waiting periods.

By being mindful of exit fees, and penalties, and understanding the insurance implications, you can effectively evaluate the potential costs and consequences of switching super funds.

Conclusion: Switching To REST Super

REST Superannuation Fund stands as one of Australia’s largest super providers based on its membership numbers.

However, the assets under management are notably smaller in comparison to funds of similar membership numbers. This discrepancy largely stems from the fund’s primary focus on the retail sector.

Consequently, young workers tend to default to REST as their super option when starting their first job in retail. Furthermore, given that retail has lower levels of remuneration than other sectors, the overall generation of super contribution per member would be less.

Is REST Super Good?nWhen comparing fees side by side, REST’s fees are cheaper than that of Hostplus but more expensive than those of AustralianSuper. Furthermore, REST has yielded lower returns for the options assessed in this REST Superannuation review.

Over the past decade, REST’s high growth return was 8.94%, trailing behind both Hostplus and Australian Super. In the Australian Superannuation landscape, several funds have undergone mergers, leading to the creation of mega funds such as Australian Retirement Trust and Australian Super.

This has led to funds growing to never seen before sizes and significant amounts of assets under management. That being said, new competition has arrived in the form of Vanguard. Vanguard launched its Australian Super fund in October 2022.

Vanguard is one of the world’s largest investment management companies with an impressive portfolio of assets exceeding $11 trillion AUD worldwide [7].

In my Vanguard Super Review, I observed that Vanguard may one day be a direct competitor to the likes of Australian Super. However, with Vanguard Super only debuting in October 2022, its long-term performance cannot yet be gauged.

Vanguard was noted for its excellent fees, which were lower than those of Australian Super.

In my recent Australian Super Review and Aware Super Review, I noticed that Australian Super exhibited some superior performances with some of the lowest fees among funds of similar sizes. Aware Super, however, had higher fees and lower performance, returns.

Given these considerations, what does this mean for REST Super?

With heightened competition from entities like Vanguard and low-fee alternatives such as UniSuper, REST must continue to provide its membership with solid returns and competitive fees. This may be easier said than done however.

This article is for informational purposes only and does not constitute as an endorsement or recommendation to purchase any specific mentioned product. Past performance is not a reliable indicator of future performance.

- https://rest.com.au/investments

- https://rest.com.au/why-rest/about-rest

- https://www.australiansuper.com/campaigns/super-moments

- https://hostplus.com.au/about-us/company-overview

- https://www.australiansuper.com/careers/our-teams

- https://www.thinkingaheadinstitute.org/content/uploads/2022/09/PI-300-2022.pdf

- https://www.vanguard.com.au/adviser/en/aboutvanguard/about-us-tab