Best Performing Super Funds Over 10 Years

Last Updated on 22 March 2024 by Ryan Oldnall

Comparing superannuation funds can be needlessly complicated, as important information is often buried or difficult to access. Fees are commonly presented in a mixture of dollars and percentages, further complicating the comparison.

Furthermore, comparing fund performance is made even more challenging due to variations in reporting frequency and data availability. For instance, some super funds provide quarterly performance data, while others present it on a monthly basis.

Moreover, specific product information is often buried deep within each super fund’s Product Disclosure Statement (PDS), making it less accessible and straightforward for comparison purposes.

In developing this article, I utilized the Australian Government YourSuper comparison tool to streamline the process [1]. This tool facilitated the identification of the best-performing MySuper funds, and I independently verified their 10-year average performances.

As a result of these manual checks, I excluded TelstraSuper. I made this decision because I couldn’t accurately ascertain their performance returns when comparing them against the other listed funds.

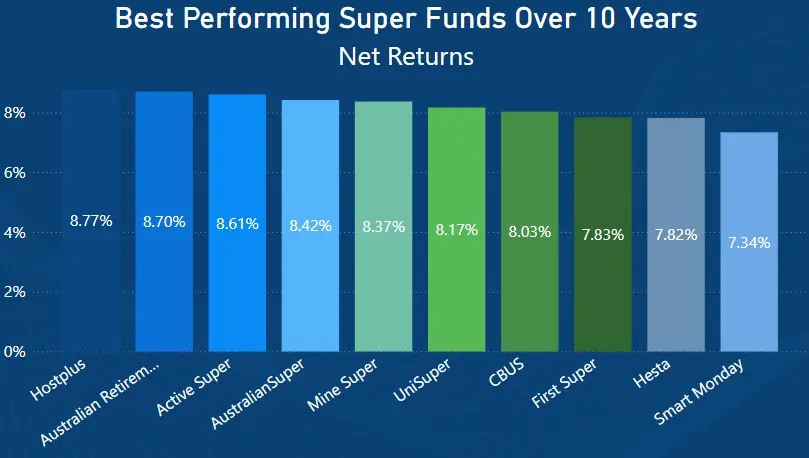

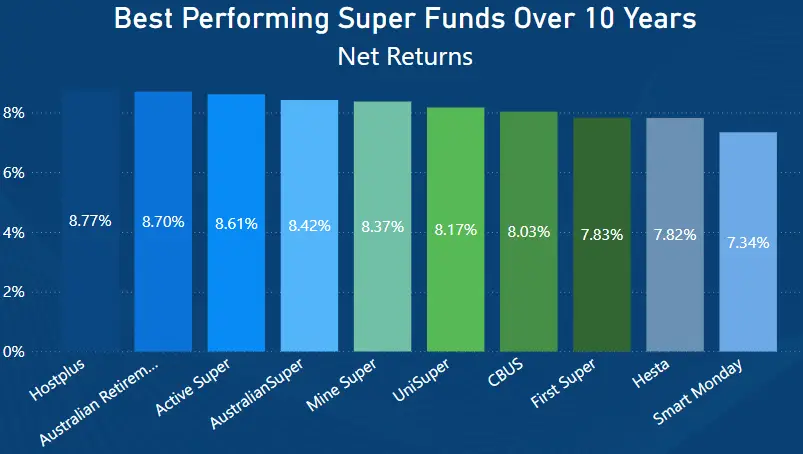

Top 10 Average Superannuation Returns Last 10 Years

For the purpose of calculating performance returns and fees, I utilized two default values: an age of 40 and a super balance of $100,000. Additionally, I only included funds available to the general public.

Top 10 Average Superannuation Returns Annual Fees

MySuper Superannuation Returns Last 10 Years

- Hostplus:

- 10-Year Avg. Return: 8.77%

- Australian Retirement Trust:

- 10-Year Avg. Return: 8.70%

- Active Super A:

- 10-Year Avg. Return: 8.61%

- AustralianSuper:

- 10-Year Avg. Return: 8.42%

- Mine Super:

- 10-Year Avg. Return: 8.37%

- UniSuper:

- 10-Year Avg. Return: 8.17%

- CBUS:

- 10-Year Avg. Return: 8.03%

- First Super:

- 10-Year Avg. Return: 7.83%

- Hesta:

- 10-Year Avg. Return: 7.82%

- Smart Monday:

- 10-Year Avg. Return: 7.34%

Top 10 Average Superannuation Returns Analysis

The above results represent net performance returns as of June 2023 and are inclusive of fees. I have highlighted fees as they are important, especially when considering a fund with higher fees but diminishing returns.

When analyzing the performance of these funds, Hostplus stands out with an impressive 10-year average return of 8.77%. Interestingly, it’s worth noting that Hostplus actually has the second-highest annual fee of $1,117.

Australian Retirement Trust follows closely behind with an 8.70% average return and an annual fee of $1,032. I have previously reviewed Australian Retirement Trust and found them to have some of the largest fees among their single super fund products.

Active Super takes the third position with an 8.61% average return and an annual fee of $1,176, which is the highest fee on the list.

AustralianSuper offers balanced performance with an 8.42% average return and a relatively lower annual fee of $712. When reviewing AustralianSuper, they had some of the lowest fees.

Mine Super also demonstrates solid performance with an 8.37% average return and an annual fee of $732.

UniSuper maintains steady growth with an 8.17% average return and a comparatively lower annual fee of $606, which is actually the lowest on the list. This is largely consistent with what I found in my UniSuper review.

CBUS and First Super deliver reliable performances with average returns of 8.03% and 7.83% respectively, coupled with annual fees of $798 and $977.

Hesta and Smart Monday complete the comparison with returns of 7.82% and 7.34% respectively. Hesta has a higher average return but also a higher annual fee of $909 compared to Smart Monday‘s $872.

These results highlight the complex trade-offs between returns and fees among the top MySuper funds.

While Hostplus offers robust net returns, it does so at a higher cost. In contrast, funds like AustralianSuper and UniSuper provide competitive returns with relatively lower fees, striking a decent balance between performance and affordability.

What is MySuper?

“MySuper” is a component of Australia’s superannuation system designed to simplify and streamline the process of selecting a super fund for employees who do not actively choose their own fund.

It was introduced by the Australian government as part of the Stronger Super reforms in 2013 [1].

Under the MySuper scheme, employers are mandated to direct the superannuation guarantee contributions for their employees into a MySuper-compliant fund, unless the employee opts for an alternative fund.

MySuper funds are intended to provide a straightforward, low-cost default option for individuals who prefer not to actively manage their superannuation investments.

MySuper fund characteristics:

The aim of MySuper is to make the superannuation system more transparent and easier to understand, thus making it more accessible to everyday Australians.

While this is the intended aim, as discussed at the beginning of this article, achieving it was somewhat difficult.

Among the top 10 funds I identified using the Australian Government tool, one fund made it challenging to find their performance and costs. For this reason, I chose to exclude them from this article.

Overall, accessing the individual performance of MySuper funds has been significantly simplified, particularly for individuals who may not have the expertise or desire to compile and manipulate data in spreadsheets.

The Government Super comparison tool offers a straightforward method for comparing funds.

Hopefully, as time progresses, the superannuation industry as a whole will be required to make information regarding performance and fees more accessible, especially concerning other single strategy products such as High Growth, Growth, and Balanced options.

This article does not serve as an endorsement or recommendation for products mentioned in the article. The information presented here is based on referenced sources and is accurate as of the date of March 16, 2024. Please note that these articles are written sometime before their publication date.

The information provided in this content is for informational purposes only and should not be considered as financial, investment, or professional advice. We recommend consulting with a qualified expert or conducting your own research before making any financial decisions.

The accuracy, completeness, or reliability of the information cannot be guaranteed, and the provider shall not be held responsible for any actions taken based on the information contained in this content.

References

- https://www.ato.gov.au/calculators-and-tools/super-yoursuper-comparison-tool

- https://treasury.gov.au/programs-and-initiatives-superannuation/mysuper